What Factors Affect Option Pricing?

Several key factors affect option pricing, including the price of the underlying asset, time to expiration, market volatility, and interest rates. Whether you use equity trading advisory services or trade on your own, understanding what drives option value helps you make smarter decisions. This guide explains each factor in simple terms.

📈 Underlying Asset Price

The price of the underlying asset is the cornerstone of option pricing. For call options, as the price of the underlying asset increases, the value of the option typically rises. Conversely, for put options, the value generally goes up as the underlying asset price decreases.

Imagine you have a call option for stock XYZ with a strike price of $50. If XYZ's stock price rises to $60, your call option is now more valuable because you have the right to buy the stock at the lower strike price.

⏳ Time to Expiration

Time is literally money in the world of options. The more time an option has until it expires, the greater the chance that it will end up in-the-money (profitable). This is known as the option’s time value.

Consider an option with 6 months to expiration versus one with 1 month left. The 6-month option has more time for the underlying asset price to move favorably, hence it's usually more expensive.

🎢 Volatility

Volatility reflects the degree to which the price of the underlying asset is expected to fluctuate. Higher volatility increases the probability that an option will end up in-the-money, thus increasing its value.

If stock ABC is highly volatile, there's a greater chance it will swing above the strike price for a call option, making the option more valuable compared to a similar option on a less volatile stock.

🏦 Interest Rates

Interest rates can have a subtle but real impact on option pricing. Generally, higher interest rates can increase the value of call options and decrease the value of put options.

With higher interest rates, the cost of carrying cash is higher, so investors may prefer to use options as a leverage tool, increasing demand and the price of call options.

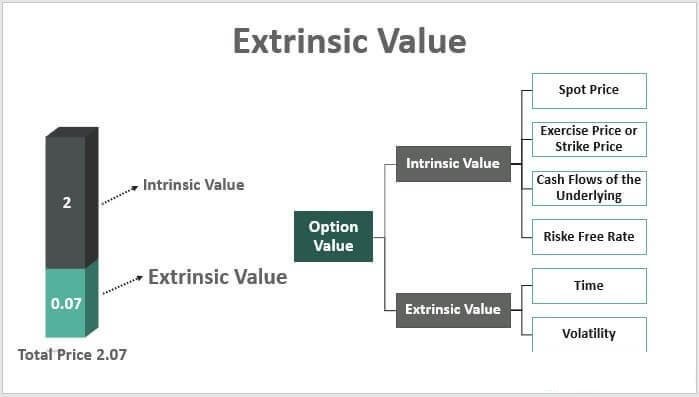

💡 Intrinsic and Extrinsic Value

Options are often discussed in terms of their intrinsic and extrinsic value. The intrinsic value is the real, tangible value of an option if it were exercised now. The extrinsic value, or time value, is the extra amount that traders are willing to pay for the possibility that the option might become more valuable before expiration.

A call option with a strike price of $50 on a stock currently trading at $55 has an intrinsic value of $5. If the option is trading at $7, the additional $2 is the extrinsic value.

🔢 Calculating Option Value

The Black-Scholes pricing model is a popular method for calculating the theoretical value of an option. It takes into account the factors mentioned above and uses them in a complex mathematical formula.

The Black-Scholes formula for a call option is:

C = S0*N(d1) - X*e^(-rt)*N(d2)

Where:

C = Call option price

S0 = Current price of the underlying asset

X = Strike price of the option

r = Risk-free interest rate

t = Time to expiration

N = Cumulative distribution function of the standard normal distribution

d1 and d2 = Calculated values based on the above factors

Understanding these factors and how they interplay to affect option pricing is crucial for any trader or investor looking to navigate the options market successfully.

Understand the underlying asset price:

- Explain how changes in the underlying asset price affect the value of options using real-life examples, such as a stock option whose price increases as the stock price rises.

Comprehend the impact of time to expiration:

- Use a hypothetical example of two call options on the same stock, one expiring in 30 days and the other in 90 days, to illustrate how the time to expiration influences option pricing.

Grasp the concept of volatility:

- Provide a fact-based explanation of how higher volatility leads to higher option prices, using a historical example of a market event that caused increased volatility and subsequently impacted option prices.

The influence of interest rates:

- Use a structured explanation to show how changes in interest rates affect the pricing of options, drawing on interest rate trends and their impact on option values.

Calculate the value of options:

- Present a step-by-step calculation of option value using a specific example, including the relevant formula and input values for the factors discussed.