Theta in Options Trading: How Time Decay Works

Theta measures how much an option’s value drops each day as it gets closer to expiration. This loss of value over time is called time decay. Theta is a key part of options pricing, and knowing how it works helps you trade smarter.

What Is Theta and How Does It Work?

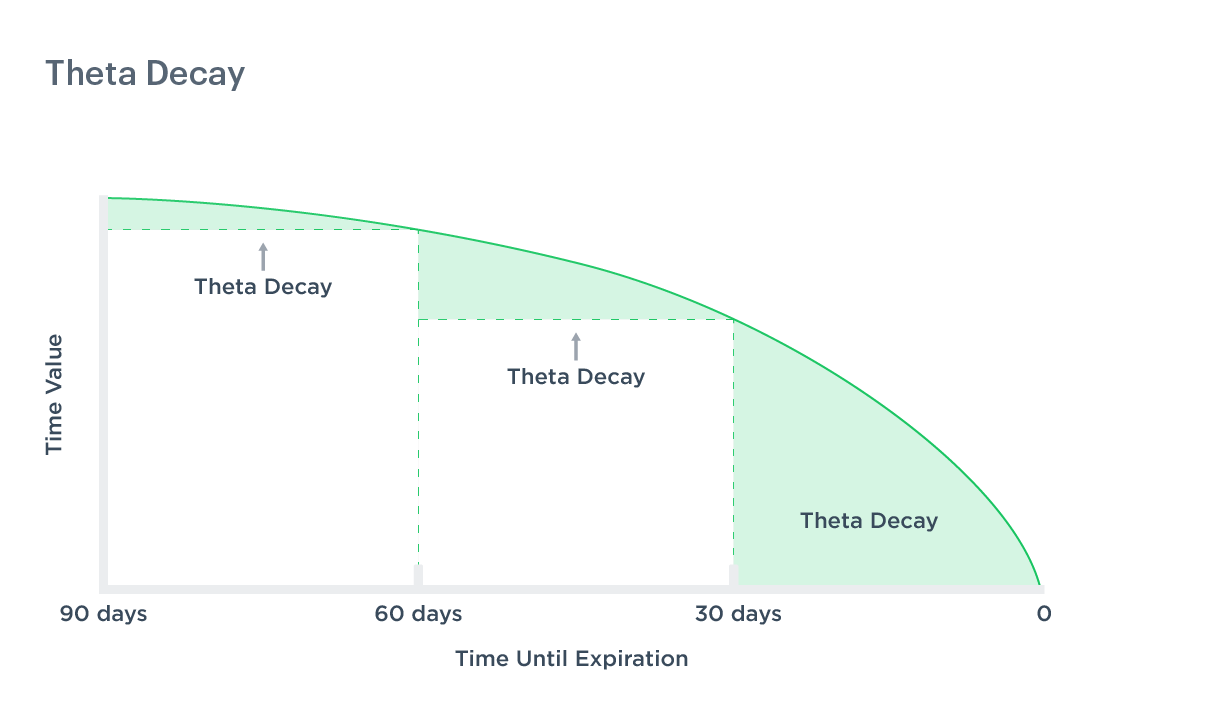

Theta measures how much an option’s price drops as time passes, when nothing else changes. Options with more time until expiration have higher value and a higher Theta. Options close to expiration have lower value and a lower Theta.

A Simple Example of Theta

Imagine you buy a call option on a stock with a Theta of -0.03. Each day, the option loses $0.03 in value simply because time passes. If the stock price does not move, the option keeps losing value. This can lead to a loss for the buyer.

How Theta Affects Your Trading Strategy

Theta helps you choose the right strategy. Traders who sell options often look for high Theta. They want to profit as the options lose value over time. Buyers, on the other hand, need to watch Theta closely because it works against them.

Understanding theta in options trading is important because it affects every trade you make. It shapes your decisions and can change how profitable your positions are. Smart traders always consider theta when planning their trades.

When you pay attention to theta, you can make better choices and improve your trading results.

Key things to know about Theta:

Theta measures time decay. It tells you how much value an option loses each day. A Theta of -0.03 means the option drops $0.03 per day. The closer an option gets to expiration, the faster it loses value.

Theta changes based on market factors. Time to expiration is the biggest factor. Implied volatility and the strike price also play a role. Theta rises sharply in the final weeks before expiration.

Theta affects buyers and sellers differently. Option buyers lose from time decay. Option sellers gain from it. Understanding this helps you pick the right trades.

Use Theta to plan your trades. Sellers can look for options with high Theta to profit from time decay. Buyers should choose longer expiration dates to slow down the daily decay.

By understanding how theta works, you can build better trading strategies and manage risk more effectively.