What Are Option Greeks?

Options trading is about more than just buying and selling. You also need to understand the key factors that drive an option’s price. These factors are called the “Greeks”, and they help you build smarter trading strategies.

📈 Delta: The Rate of Change

Delta measures how much an option’s price may change when the underlying asset moves by one point. For example, a delta of 0.5 means the option’s price will change by 0.5 for every 1-point move in the stock or index.

Example: If BankNifty moves from 35000 to 35001, and the option delta is 0.5, the option price will increase by 0.5.\n🕒 Theta: Time’s Impact on Value

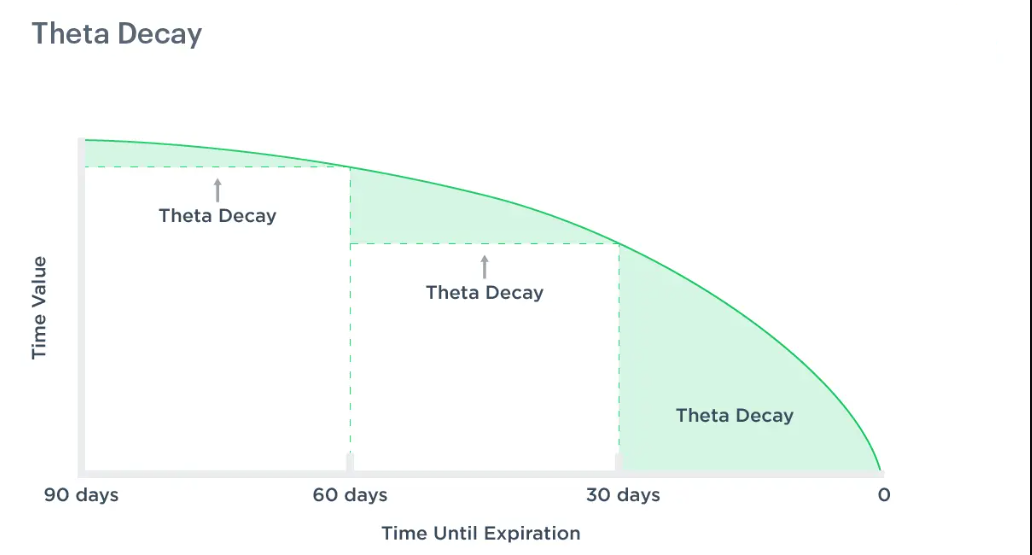

Theta measures how much value an option loses each day as time passes. This is called time decay. Options lose value the closer they get to their expiration date.

Example: If an option has a theta of -0.03, its price will decrease by 0.03 every day, all else being equal.\n🔍 Vega: Sensitivity to Volatility

Vega measures how much an option’s price changes when market volatility shifts. A higher Vega means the option’s price is more sensitive to changes in volatility.

Example: If the implied volatility increases by 1%, an option with a vega of 0.10 will increase in price by 0.10.\n🏛️ Rho: Interest Rates’ Influence

Rho assesses the impact of interest rate changes on an option’s price. It’s less commonly used but important for long-term options.

Example: If interest rates rise by 1%, an option with a rho of 0.05 will increase by 0.05 in price.\n🔄 Gamma: The Rate of Delta Change

Gamma measures how fast Delta changes when the underlying asset price moves. It tells you the acceleration of an option’s price change.

Example: If gamma is 0.10 and delta is 0.5, and the underlying stock moves by 1 point, the new delta would be 0.6.\nHow to Use Greeks in Your Trading Strategy

The Greeks help you create smarter options trading strategies. For example, a high Theta value means holding an option near expiration may lose value quickly. A high Vega can help you trade based on expected market volatility.

Balancing Delta for Hedging

By balancing Delta, traders can hedge their positions to reduce risk. A Delta-neutral strategy aims to have the total Delta of a portfolio equal to zero.

Profiting from Theta Decay

Selling options lets you benefit from theta decay. As time passes, options lose value, which works in the seller’s favor. Learn more about theta decay and time erosion.

Using Vega to Trade on Volatility Changes

Traders may buy options with a high Vega when they expect volatility to rise. They may sell options when they expect volatility to fall.

Using Gamma to Adjust Your Trades

A high Gamma position needs more frequent adjustments to stay delta-neutral. This can affect your trading costs and potential profits.

Master the Greeks for Smarter Options Trading

The Greeks give you a clear way to understand options pricing and risk. By learning these metrics, you can predict price movements and build strategies that match the market. Whether you trade BankNifty options or other instruments, the Greeks are valuable tools for every options trader.